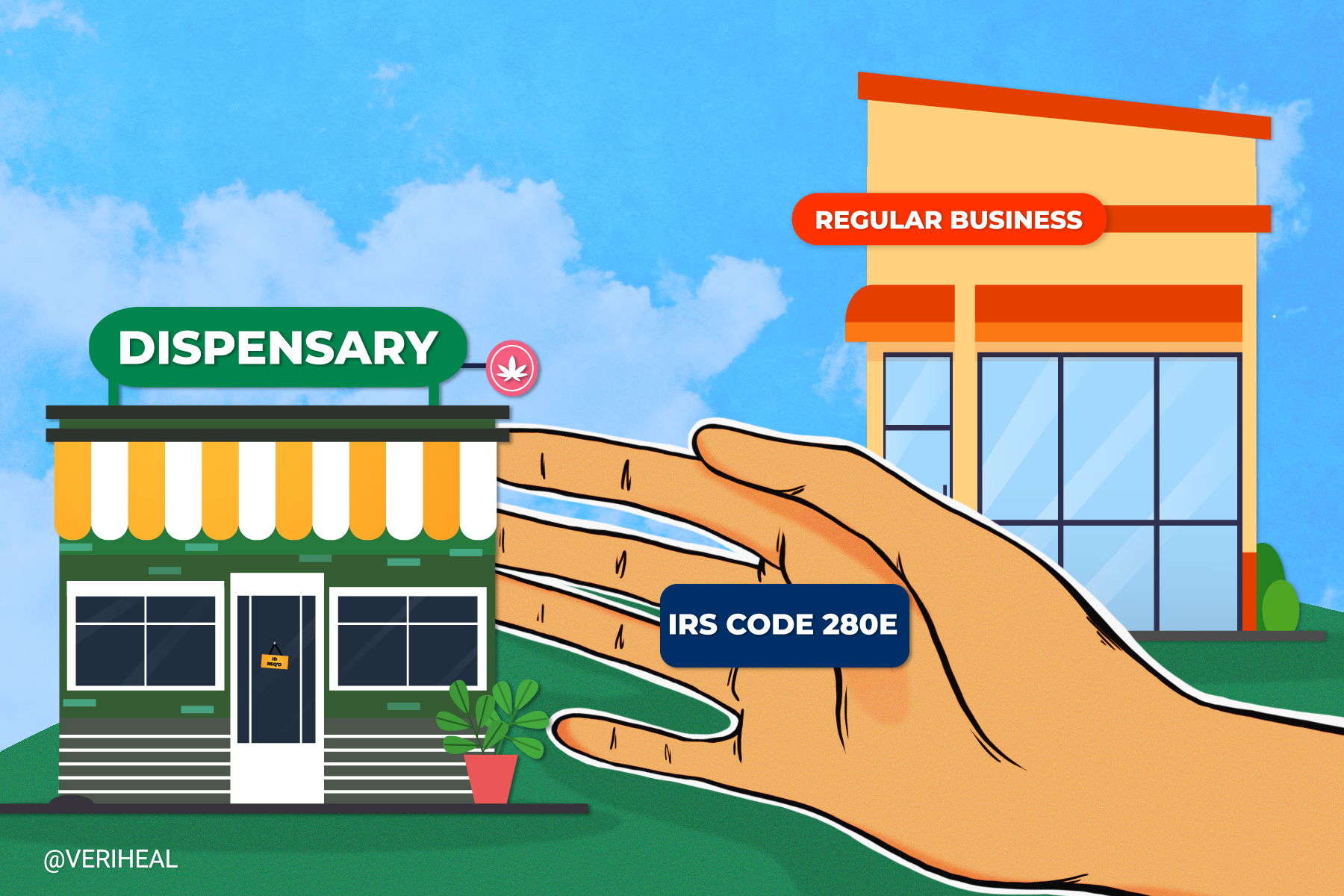

Cannabis is a profitable business and always has been. Throughout prohibition, those who supplied consumers and patients from seed to sesh had to operate utilizing cash. Unfortunately, even today, cannabis businesses operating in compliance with local and state laws are still having to operate in the same manner with the added bonus of IRS 280E tax code headaches.

While some cannabis businesses have been able to work with local credit unions and state-chartered banks, they have done so while presenting a significant challenge and risk for all parties involved. Since cannabis is still illegal on the federal level, banking and financial institutions are unable to work with cannabis businesses operating in state-legal markets. This has caused substantial headaches and risks for businesses over the years.

Speaking of headaches, IRS tax code 280E is one pain in the butt that almost every cannabis business will place at the top of their yearly business hurdles. This tax code was enacted as a result of a court case in the 1980S. This case originated after “a convicted cocaine trafficker asserted his right under federal tax law to deduct ordinary business expenses”, according to a release from the National Cannabis Industry Association.

IRS Code 280E is Enacted for Criminals Not Compliant Businesses

By enacting 280E, Congress was able to put in place regulations to prevent illegal drug dealers from deducting expenses such as employee salaries, rent, utilities, and advertising. Today, however, there are thousands of legitimate cannabis businesses operating in compliance with state laws within regulated markets that are suffering from a tax code that was meant to target illicit activity and that is highly in need of reform.

By not allowing these business deductions, it increases the amount of taxable income a business must pay taxes on which can result in significant tax debt. Especially considering that the federal tax rate averages around 21% for most businesses but for cannabis companies that must adhere to code 280E, they could face federal tax rates in the range of 40 to 80%.

According to attorney James Mann, “the 16th amendment says you can have an income tax. And the first argument is that since 280E results in a tax that’s not on income, it’s not an income tax, so therefore it’s unconstitutional.” In 2020, Mann filed an appeal with the US Court of Appeals for the Ninth Circuit in San Francisco. This was on behalf of Harborside Health Center, an Oakland, California-based cannabis retailer.

The way 280E was written, is directly related to the “trafficking” of cannabis-derived products. The greatest impact is felt by businesses operating within the retail sector of the industry. Businesses operating in the cultivation, processing, extraction, infusing, and retail verticals are all subject to this tax code. 280E can have applicable aspects anywhere that wholesale cannabis product changes hands.

COGS for Cannabis Businesses is Confusing

Investopedia.com defines COGS or Cost Of Goods Sold as “the cost of acquiring or manufacturing the products that a company sells during a period, so they only cost included in the measure are those that are directly tied to the production of products, including the cost of labor materials, and manufacturing overhead.”

Per IRS tax code 280E cannabis businesses are only allowed to deduct expenses related to inventory as Cost Of Goods Sold. Knowing what can and cannot be deducted as COGS can be quite confusing for cannabis businesses. Here is a quick overview.

- Any expense that is not part of COGS is not considered deductible.

- Cannabis cultivators are able to claim deductions for raw materials such as clones, seeds, and fertilizer.

- Indirect production costs such as those incurred for repairs and maintenance of production equipment, water and electricity costs utilized to cultivate cannabis, grow supplies and packaging, cost of quality control and inspection as well as indirect wages such as those for supervisors are deductible.

- For cannabis cultivators, direct labor costs incurred before the sale of products for things such as cleaning, curing, trimming, packaging, and inventory can also be deducted as COGS.

- Cannabis resellers such as dispensaries are able to claim things such as transportation costs including those incurred to travel to purchase cannabis, ship cannabis, or transport cannabis.

- Dispensaries can also claim deductions for electric bills under COGS with the exception of any electricity used within sales areas.

In order for cannabis businesses to stay compliant with this tax code, it takes vigilance. Working with a certified public accountant also known as a CPA is highly advised for cannabis businesses. This is because in most cases tax audits are something that all cannabis companies will eventually face so it is best to keep clear and concise accounting records so that you are prepared when the time comes.

Has IRS Tax Code 280E been a pain for your business? Let us know about your experiences in the comments below to keep the conversation going!

Author, Share & Comments